What is a Mortgage?

Everything you need to know about mortgages.

Everything you need to know about mortgages.

A mortgage is simply a financial transaction. It’s a promise, with official documentation and government regulations, that you will repay a large debt. Although some people would say that the mortgage process can be a headache, these loans can make owning your dream home possible. Homeownership is a big undertaking, however. That’s why it’s best to be prepared and work with a lender you trust.

Mortgages, similar to the people they help, come in many varieties. There are options for low-income borrowers, or even people purchasing mega dream homes valued in the millions. When it comes down to it, your mortgage will exist as a piece of paper and a promise. When you start thinking seriously about your mortgage, one of the first things you will need to know about is rates.

Simply put, a mortgage rate is the interest charged on a mortgage loan. Mortgage rates are changing constantly based on market conditions.

Market conditions include such things as the economy, characteristics of the housing market, and the federal monetary policy. However, your individual financial health will also affect the interest rate you get on your loan. Understanding what affects interest rates is challenging; however, understanding how interest rates affect you is simple.

The lower your interest rate, the cheaper your loan will be. If you are aiming to get the lowest interest rate, you should think about the type of loan you’ll use, your qualifying factors, and the condition of the market.

The truth is, if you have a strong financial profile, your loan will cost you less. So if you want to have a lower rate, you should increase your credit score, lower your debt, and save a healthy down payment. This will put you in excellent standing and make you a more attractive borrower.

Sometimes using specific government-backed mortgage products will give you access to a better rate. FHA, VA, and USDA home loans are great examples of products with typically lower prices.

Another way you can make sure you get the best rate possible is by paying attention to the housing market itself. If it’s a buyer’s market and there is ample housing inventory, it may be an excellent time for you to lock in a low-interest rate. The housing market moves cyclically, so it is only a matter of waiting for the right time to purchase. Something often confused among homebuyers is the difference between APR and interest rate. While they are both a rate, there are differences between the two. We’ll explore the details of APR next.

Even though the annual percentage rate (APR) is calculated as a rate, it is different from your loan’s interest rate. The annual percentage rate is the overall cost of a mortgage, including interest, closing costs, and other associated fees over the lifetime of the loan. Lenders use the formula below to calculate APR.

Lenders are required to disclose the APR because of the Truth in Lending Act. When you receive your loan estimate from your lender, it is important to turn to page 3. This is where you can see your loan’s APR. You will see APR is a slightly higher rate because it is the added costs on top of the interest rate. Also, you will see how much interest you will pay over the lifetime of your loan. If you are looking for more ways to secure an even lower rate, and you have already submitted an application, you may want to ask your mortgage consultant about buy down options.

Another great way to lower your interest rate and APR is by using mortgage or discount points. One mortgage point would represent 1% of the loan amount. Each point you purchase will buy down your mortgage rate. Over time, the lower rate can save you money. That’s right – mortgage points help you lower the monthly cost of your loan, but be careful! If you plan on selling the home before you break even, the amount you save may not be more than the amount you spent.

These discount points or basis points are offered upfront and written into the contract. Be careful when you get quotes from other lenders because they may be including discount points into their interest quote. It is essential to read the fine print.

If you are interested in seeing how much you can save using discount points, ask your mortgage consultant about a buy-down agreement.

Your Loan-to-Value (LTV) represents the value of your home compared to the amount you owe on your mortgage loan. For example, if you are purchasing a home that is appraised at $200,000 and your loan amount will be $180,000, your loan to value would be 90%.

LTV is a measurement that lenders can use to calculate risk. So if you pay more down, you would have a lower LTV, which could also translate to better interest rates and easier qualifications. This doesn’t mean you need a large down payment to qualify for a mortgage. It’s not uncommon for borrowers to obtain loans with LTVs as high as 97%. There may be more flexibility with government-backed products like FHA, USDA, and VA home loans.

Qualifying for a mortgage is much easier than a lot of people realize. Barriers to homeownership, low credit score, or no down payment can all be overcome with financial planning or assistance. To discover what the best option is for you, you can start by getting pre-qualified.

When you submit your loan application, an underwriter will weigh different qualifications as they assess your creditworthiness. They take a look at the full picture and examine various factors like employment history, income level, debt-to-income ratio, credit history, and down payment.

In general, a lender will want to see a work history that stretches back two years. Not only do lenders want to know that you have consistent income, but they also want to be sure that your income will support a mortgage. It’s also crucial that you are effectively managing any other outstanding debt. Mortgage debt is a huge financial commitment and could dramatically change your monthly responsibilities. The underwriter will review many documents to assess your credit worthiness to make a determination for loan approval, including tax returns, pay stubs, and credit reports.

For the least expensive loan, you would want to have a healthy down payment. However, you have options that could allow you to qualify with 100% financing. Government-backed programs such as USDA and VA give borrowers low down payment loan options. Also, the FHA allows eligible borrowers to qualify with as little as 3.5% down. These aren’t the only programs that help homebuyers afford their down payment though.

Many DPA programs throughout the country can assist with down payments. Each program is worth investigating because their qualification factors may be different. Your income, homeownership history, and the location of the property are only some examples of factors that may limit your participation in the program. For more information on Down Payment Assistance programs near you, visit our DPA page.

The minimum credit score required for a qualified homebuyer depends on the mortgage program you use. With FHA, VA, and USDA home loans, the minimum credit score they need is 580. With a conventional program, however, the minimum is 620. If you are interested in finding out what your credit score is, you can use any of the three major credit bureaus.

Your debt-to-income is a generic measurement of your financial situation. You can calculate it by taking your monthly expenses and dividing them by your monthly income.

A healthy financial situation means you aren’t drowning in debt, so a lower DTI is preferred. It’s recommended that you keep your DTI below 43%. Usually, borrowers with DTI over 43% are considered riskier, although there are exceptions made. Lenders could approve borrowers with DTI as high as 47% using specific mortgage programs.

As a homeowner, you want to continue saving money. So make sure you don’t overextend your budget on a mortgage.

You can get a mortgage from a lender, bank, or broker. A lender and a bank are both financial institutions, whereas a broker operates like a private contractor. Working with a lender offers many benefits, including competitive rates, plenty of product options, and flexible qualifying guidelines.

When you apply for a loan, a lender is going to ask for personal information to verify your data is accurate. You may need to provide private information to your lender, such as your social security number, tax records, or bank statements. Depending on your situation, a mortgage advisor might ask you about credit events from your past, and you may have to explain why a credit event is on your history.

No matter what organization you choose to help you fund your dream home, you’re going to work directly with one person. This person represents the lending institution and will help you originate your loan. This type of mortgage expert is referred to as a loan officer or a mortgage consultant.

You can start your search by looking at lenders and mortgage consultants in your area. Working with someone close by will be helpful. Feel free to ask for recommendations from friends and family. Another option is to start by visiting a lender at their office or calling them up. If you do prefer to get a loan online, then make sure the lender you work with provides that option. With On Q Home Loans, you can start your mortgage journey from your phone by downloading a mobile loan app.

Pre-qualification is when a bank or lender will ask you to provide them with a current snapshot of your financial health. This is going to include your credit, score, debt, income, and assets. Once the lender can review your financial standing, they give you an estimate of the amount you can borrow.

Pre-approval is the definitive answer in demonstrating your creditworthiness. Pre-approval is also the next step after pre-qualification. There is so much more that goes into getting pre-approved, and because of this, it carries more authority.

To get pre-approved, you’ll need to fill out an official mortgage application, and you must provide your mortgage lender with the required documentation so they can conduct a complete check on your financial history and current credit scores. Your lender will be able to pre-approve you for a specified mortgage amount after reviewing your overall financial health. Another benefit of pre-approval is that you’ll have a much better idea of the interest rate you’ll be charged. Your loan interest rate is often based on your credit score, and after pre-approval, you could have an opportunity to lock in an interest rate.

As a potential homebuyer, you will find that most lenders offer a few popular loan types: Conventional, FHA, and VA loans. An additional loan type available for eligible rural and suburban homebuyers is a USDA Home Loan. Each loan is designed to benefit homebuyers in different ways. Not every loan type will be right for you, so it’s essential you get all the info you need upfront.

A conventional mortgage is a mortgage product that follows conforming guidelines and is not guaranteed or insured by a government organization. Conventional home loans are available through individual lenders and may be sold to the two government sponsored enterprises, Fannie Mae, or Freddie Mac. You can find out more about a conventional mortgage on our home loans page.

An FHA loan is a loan that’s insured by the Federal Housing Administration. The FHA does not lend money; it just backs qualified lenders in case of mortgage default.

Visit HUD.gov for more info on FHA loans: https://www.hud.gov/program_offices/housing/fhahistory.

What are the benefits of an FHA loan?

If you are light on capital or have a lower credit score, an FHA loan might be a good fit for you. FHA loans can also benefit an individual who has had a recent derogatory credit event such as foreclosure, bankruptcy, or a short sale. As long as you have re-established credit, an FHA loan requires shorter waiting periods to be eligible for financing compared to conventional loans for borrowers with a recent derogatory credit event. If the borrower needs assistance in qualifying, FHA loans let relatives sign as non-occupant co-borrowers as well.

The United States Department of Agriculture (USDA) issues USDA rural development home loans. This home loan can provide 100% funding, but are limited to specific regions and have household income restrictions. You can find out more about a USDA mortgage on our home loans page.

VA loans are mortgage loans that are insured by the U.S. Department of Veterans Affairs or VA. These loans are offered to active duty military or veteran service members based on how long they served. It’s important to distinguish that the VA does not lend money. The VA guarantees the loan when it is closed, protecting the lender if the borrower fails to repay the loan. Both the borrowers and the lenders must meet qualifications to be eligible for a VA loan.

A loan made above the conforming county loan limits amount is called a jumbo loan. U.S. home prices have risen so high in some areas that many buyers need jumbo loans to finance them. The term jumbo in the home loan world refers to loans that exceed the limits set by the government-sponsored enterprises Freddie Mac and Fannie Mae. This makes them non-conforming loans. Jumbo loans generally have a slightly higher interest rate. Jumbo loans are riskier for lenders as they involve more money and don’t have mortgage insurance. All non-conforming loans, including jumbo loans, have guidelines set by the lending institution that is underwriting the loan.

An adjustable-rate mortgage (ARM) allows you to secure your loan with a lower interest rate, but at the risk of your rate going up after a few years. ARM loans typically come with 5/1 or 7/1 terms. This means that after five or seven years, your interest rate may change according to the market at that time. These types of mortgages can be great for short term home purchases, but ARM loans are a risk. You can find out more about the benefits and disadvantages of an ARM program on our home loans page.

Fixed-rate mortgages offer a fixed payment over time and usually come with 15 or 30-year loan terms. The interest rate is fixed for the life of the loan and won’t change. Still, a majority of homebuyers want the security of a consistent payment, so they choose to go with fixed-rate mortgages. You can learn more about this mortgage option on our home loans page.

These types of loans allow you finance renovations and improvements on your home, and simply roll the costs into a new mortgage. The products FHA 203K and Fannie Mae Homestyle offer fixed-rate options. Remodel your home with ease using a home improvement loan. Learn more here.

A one-time construction, otherwise known as a construction-to-permanent loan allows you to purchase a production or custom construction home with one trip to the closing table. The program enables you to purchase using FHA, VA, USDA, and Conventional financing. If you are thinking about building your dream home instead of buying it, you may consider the simplicity of a one-time construction loan.

Financing is offered on manufactured homes for doublewide or singlewide homes built on or after June 15, 1976, and offered on FHA, VA, and Conventional loans. USDA will only allow new manufactured homes. Manufactured home loans allow for low down payment options. The property must meet manufactured home guidelines and are considered an affordable housing option.

Non-QM stands for a non-qualifying mortgage. This type of mortgage is used for borrowers who may not qualify for traditional mortgage standards set by the Consumer Financial Protection Bureau. Non-QM loans give opportunities for homeownership to borrowers who are self-employed, investors, or who have a recent negative credit event.

A reverse mortgage is a mortgage option designed for you to be able to take cash out of the equity in your home, and then the equity is converted into a cash payment to the borrower who is 62 years or older. This is a great option for borrowers who are retiring on a fixed income. No payments are required until you sell the home or pass away. A reverse mortgage isn’t something that is right for everyone.

Would you rather pay off your new iPhone over 12 months or 24 months? In the end, you’re paying relatively the same amount for the same thing; it’s just going to cost you a different amount per month. This is a straightforward analogy for the difference between 15-year and 30-year term fixed-rate home loans.

With a 15-year fixed-rate mortgage, you’ll have the satisfaction of paying off your loan in 50% the time it would take you with a 30-year fixed-rate mortgage. On the other hand, a 30-year mortgage will cost you less month to month.

Something to consider is that with the shorter 15-year term versus a 30-year term, you’ll pay less overall interest on your loan. You’ll also be building up your home equity much faster with a 15-year loan. While these are nice things, you may want to consider the consequences strongly. Your mortgage payment will be higher as it is amortized over a shorter term. If you might not be able to afford this, it may be safer to go with a 30-year fixed-rate mortgage term.

Loan limits restrict the maximum amount of money a homebuyer can borrow to purchase or refinance a home. Government Sponsored Enterprises or GSEs cap the dollar amount of a mortgage based on the county the property is located in using a percentage of the area medium prices for homes in the county the home is located in. This, of course, covers the lenders and gives them a better chance of avoiding a borrower defaulting on their mortgage.

Conforming conventional loan limits change from area to area and from year to year. This year, in 2020, and in most of the mainland U.S., single-family homes have a conforming loan limit of $510,400 and may be more in high-cost areas. The FHA loan limit in most counties is $331,760. These loan limits are set by using a percentage of the area medium price in the county the home is located in.

VA Loan Limits no longer apply to qualified veterans who have full VA loan entitlement! The VA county loan limit in most areas for borrowers with 100% entitlement can exceed the county loan limit of $510,400 with On Q Home Loans up to $1,500,000 as long as they qualify.

Loan limits still apply to borrowers with more than one active VA loan. Keep in mind that borrowers who have defaulted on a previous loan are only eligible for partial entitlement as long as the lender can obtain a 25% guarantee on the loan. Usually, this 25% guarantee is fulfilled by requiring additional funds for down payment.

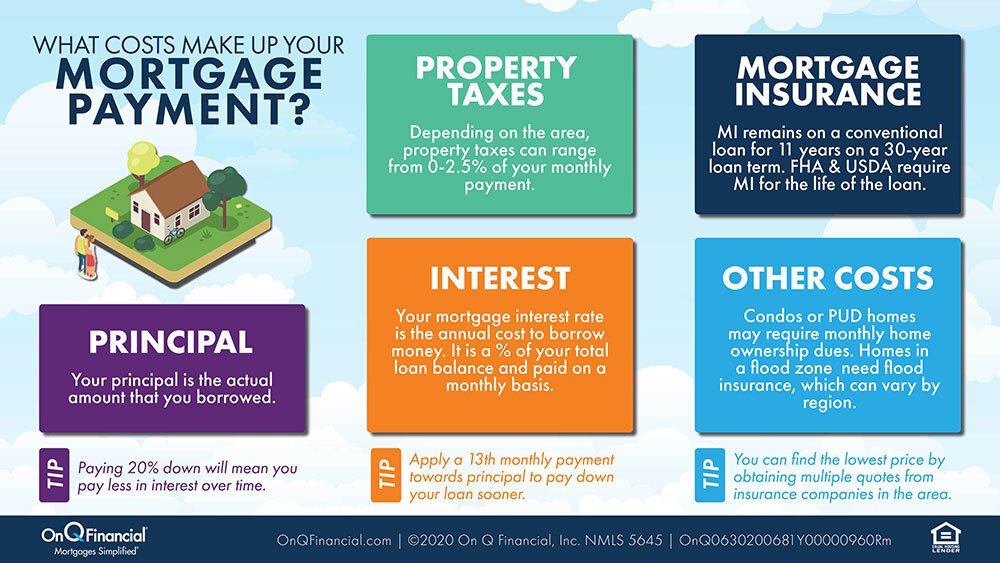

You’re going to be paying your mortgage every month so you might as well know what’s in there. There are four parts that make up your monthly mortgage payment: principal, interest, taxes, and insurance.

A loan’s principal balance is the original loan amount minus the portion of payments that have been made against the principal balance.

Mortgage interest is paid in addition to the principal loan amount borrowed. It’s the cost charged for borrowing money.

It’s common to find that the property tax will also be added to your monthly mortgage payment. Your lender will just hold onto this money in an escrow account. When the property tax on your mortgage is actually due that year, that’s when your lender will take that money out of the escrow account and use it to pay the property tax.

There are different types of insurance you need to know about when obtaining a mortgage.

When you take out a mortgage, the lender will require you to take out hazard insurance (aka homeowners insurance) to protect their investment.

Private Mortgage insurance, (PMI) on conventional loans may be included in your monthly payment if you are putting less than 20% down. FHA and USDA require a monthly mortgage insurance payment, which will be included in your total monthly payment.

If your home is in a designated flood zone that requires flood insurance, the monthly flood insurance premium will be included in your payment.

An insurance policy may be required on your mortgage if you pay less than 20% down. Mortgage insurance protects your lender if you default on the loan. In most cases a premium is calculated annually based on a percentage of your loan, and charged on a monthly basis. Depending on the program you use, you may be required to pay not only a monthly premium, but an upfront premium.

Depending on the program you use, your mortgage insurance may be called private mortgage insurance (PMI) or a mortgage insurance premium (MIP). You’ll need PMI when you obtain a conventional mortgage, and you’re putting less than 20% down. If you are obtaining an FHA or USDA loan though, you have to get a MIP. With VA loans, you don’t get mortgage insurance, but instead, you pay what’s called a funding fee.

Mortgage insurance saves you for a while if you begin to miss payments on your loan. The money you’ve paid towards insurance will effectively satisfy, for a short amount of time, your lender’s need for debt payment. Be sure that you understand mortgage insurance does not protect you from having your home go into foreclosure. You have to find a way to get back on track and start making your mortgage payments again before the grace period initiated by your mortgage insurance is over.

PMI is not a requirement for every mortgage, but for some programs such as FHA and USDA you will be required to pay MI for the lifetime of the loan. A way to remove mortgage insurance is refinancing into a loan with an 80/20 LTV or lower on a conventional mortgage. In other words, paying 20% down or more on a conventional mortgage is the only way to avoid paying for mortgage insurance or funding fees.

The big draw of a conventional mortgage is the low down payment options. Borrowers can pay as little as 3% down with a conventional mortgage. Although if you make a low down payment you are required to pay for private mortgage insurance or PMI.

With all FHA loans, you have to pay a mortgage insurance premium or MIP. You’ll pay a 1.75% premium upfront. You also have to pay for an annual premium. Your annual premium can be anywhere from .45%-1.05% depending on your LTV, loan term or loan amount of the average balance remaining for that year. If you put down less than 10%, you’ll pay a mortgage insurance premium for the entire timespan of your FHA loan. However, if you can put down any more than 10% initially on your FHA loan, you’ll only have to pay MIP for 11 years.

The U.S. has loans available for military service members, some members of the National Guard, and in certain cases the surviving spouses of veterans who’ve passed on. These loans are called VA loans, because they are funded by Veteran Affairs. These loans have low-interest rates. They also have options for no down payment at all. You don’t need to purchase mortgage insurance, but you’ll most likely have to pay a funding fee if you don’t. This funding fee depends on whether or not you’ve received a VA loan before. Additionally, your status in the service, whether you’ve sustained certain injuries during your service, or if you’ve incurred disabilities from injuries during your service, can determine if you have to pay the funding fee. The funding fee is anywhere from 2.3%-3.6% as of 2020.

USDA loans do require you to have mortgage insurance. You’ll pay for this in a combination of two ways. There is a one-time upfront guarantee fee you have to pay. In 2020, this upfront guarantee fee is 1%. Then there is an additional annual fee that is divided up into your mortgage payment every month. In 2020, this annual fee is .35%. This annual fee lasts the entire duration of the USDA loan life. These percentages can change year to year, but once you close your USDA loan, it will not change because of any yearly percentage rate fluctuation.

The truth is, acquiring a mortgage comes with costs. Closing costs are the fees you pay for closing a mortgage. Before finally closing your mortgage, you’ll sign all of your mortgage documents and finalize the papers that make you the effective owner of your new home. Every step of the way to this moment, many people were helping move the process along. Your closing costs are essentially the costs of services given.

Your closing costs will be 2%-5% of your home purchase price, with varying factors impacting that percentage. Some of these variables include the state you close in, the type of loan you receive, and even your lender. You can look for an itemized list with specific closing fees on your loan estimate and closing disclosure.

If you were beginning to worry that the closing costs are stacking up against you, you’re not alone. Utilizing the following suggestions can help make closing easier by minimizing fees. First, know your options and know that you can choose which vendors and agents will help you close your home. Next, try to reduce the number of prorated days between closing your loan and paying your mortgage. You may also ask the seller of the home if they are willing to cover some of the closing costs for you, as many sellers are eager to close. Lastly, review your final closing documents to ensure fees are correct and fair. The guide below explains the costs you may see on your closing disclosure.

It’s important to know that there is a difference between your lender and your servicer. Your lender is the one who originates the loan, whereas your servicer is who you will be making payments to. The reason that these organizations are often different for the borrower is because of the mortgage-backed securities market.

Although your loan is still unpaid for, your mortgage has a lot of value. The interest you are paying on the loan is an income revenue that investors can capitalize on. Whichever investor your loan gets sold to is who you will be paying month to month.

Fannie and Freddie both purchase mortgages from different financial institutions. Fannie purchases loans from credit unions, big banks in the commercial finance industry, and mortgage brokers. Freddie, on the other hand, buys the smaller loans from original lenders who are sometimes referred to as “thrift banks.” Both Fannie and Freddie are a vital part of the mortgage industry. Their role in moving money through the US Housing economy helps to assure that mortgages are affordable and accessible to homebuyers.

Yes, you have a multitude of loan opportunities to choose from when considering refinancing, but it’s crucial to weigh all of your options. Factors such as how much longer you plan to stay in your home, your financial goals, and your credit profile should be considered when deciding whether or not to refinance and when.

Your servicer will send a mortgage release. This document, otherwise known as mortgage satisfaction paperwork, shows that your loan is paid in full and the bank no longer owns a lien against the house. Once you have officially paid off your home and your mortgage is free and clear, you are going to have to start paying any monthly charges, such as insurance, and property taxes yourself.

Forbearance is a way to relieve mortgage payments for a period of time. Your servicer is able to reduce or suspend your required payments. This gives homeowners the opportunity to get back up on their feet if they suffer a loss of income or are unable to make regular payments. When you contact your servicer, be prepared to ask some questions. Here is a list of questions suggested by the CFPB:

Forbearance can be a great option for struggling homeowners, but it is not always the best one. While your loan sits in forbearance, it will continue to accrue interest, and that large debt isn’t going anywhere. If you are able to make smaller payments, you may want to consider continuing. Your servicer may be able to work with you, so contact them and ask.

This signed document is your promise that you’ll repay your loan, with interest, over an agreed period and at a specified rate. A mortgage note is also known as a promissory note. You will sign both a promissory note in order to secure your loan, and a deed of trust to transfer ownership.

Banks or major lenders aren’t the only people able to issue a promissory note. You may be surprised that anyone else lending money with a contract is also using a promissory note. An official promissory note only requires a promise to repay a loaned amount and both parties’ signatures.

If there’s a physical, tangible item involved in the loan like a home or a car, you’re signing a secured promissory note. Any item of value that you’re using the loan to purchase is considered collateral, and this collateral secures the loan.

On the other hand, if you’re signing an unsecured promissory note, there isn’t a physical item of collateral involved. With an unsecured promissory note, the loan is lent to you purely with the understanding that you will be able to pay back the full amount plus interest. You’ll find that major banks and commercial lenders use secured promissory notes when dealing with loans for large amounts of money.

Unsecured promissory notes are generally used in instances of small loan amounts between relatives, friends, or banks.

Mortgages do not have to be complicated. When it comes down to it, a loan is simply a promise to repay a large amount of money, and they are easier than ever to obtain. Not only are there plenty of loan options, but at On Q Home Loans we make it easier with our mobile loan app that allows you to upload your documents securely from your phone. If you are thinking about taking the next steps with your mortgage journey, the answer seems simple.

The following loan scenario is only an example. Actual amounts, fees, and rates vary depending on each individual borrower’s situation and additional factors. Loan example is based on a loan amount of $500,000, 30-year fixed conventional mortgage loan with a 3% down payment of $15,000 and estimated closing costs of $3880. Interest rate of 4.375%, APT of 5.437% and an estimated monthly payment of $2,975.96. All amounts shown are estimates provided for educational and comparison purposes only and will vary for each loan. Rates and fees are subject to change at any time. This is not a commitment to lend or extend credit. Loan approval is subject to applicant’s qualifications for a loan program. Information is subject to change without notice. The material provided is for informational and educational use only.

The information is considered accurate and reliable at the time of being published. Please contact your On Q Home Loans Mortgage Consultant for more information. On Q Home Loans is an Equal Housing Lender. NMLS 5645