How to Make an Offer on a House

Don’t get caught up in the money; there is more to a purchase offer than just a price tag on a house

Don’t get caught up in the money; there is more to a purchase offer than just a price tag on a house

Sometimes called an offer letter, your purchase offer will be your introduction to the sellers, so you should ensure your agent is prepared with everything you want to include. Before jumping in, though, you will need to know what you can afford so that you shop for something within your budget. Contact a Mortgage Consultant to get a pre-qualification.

Assuming you have your pre-approval and are ready to put an offer on the house, you’ll want to discuss the following items with your agent as they will be the ones contacting the seller. Within the purchase agreement, the agent will spell out the terms of your contract.

Talk with your agent about:

Although every case is unique, responses will usually fall into one of these categories: accept, decline, or counter offer.

If your seller liked your offer and agreed to any terms or contingencies within, they will respond with an acceptance. After the purchase offer is signed, you are officially under contract! This is cause for celebration as it means you have secured your dream home!

On the other hand, sellers will sometimes respond with a declination. The seller will usually express any issues they had with the purchase offer allowing you to make another offer. However, other times, sellers have received a better offer, so make sure you read on to make sure you put forth the best offer!

The most likely response is a counteroffer. A counteroffer is issued when the seller is interested in selling the home to you, but they have some changes they would like in the purchase agreement. A counteroffer can be as simple as declining a specific contingency or suggesting you match another offer they have already received.

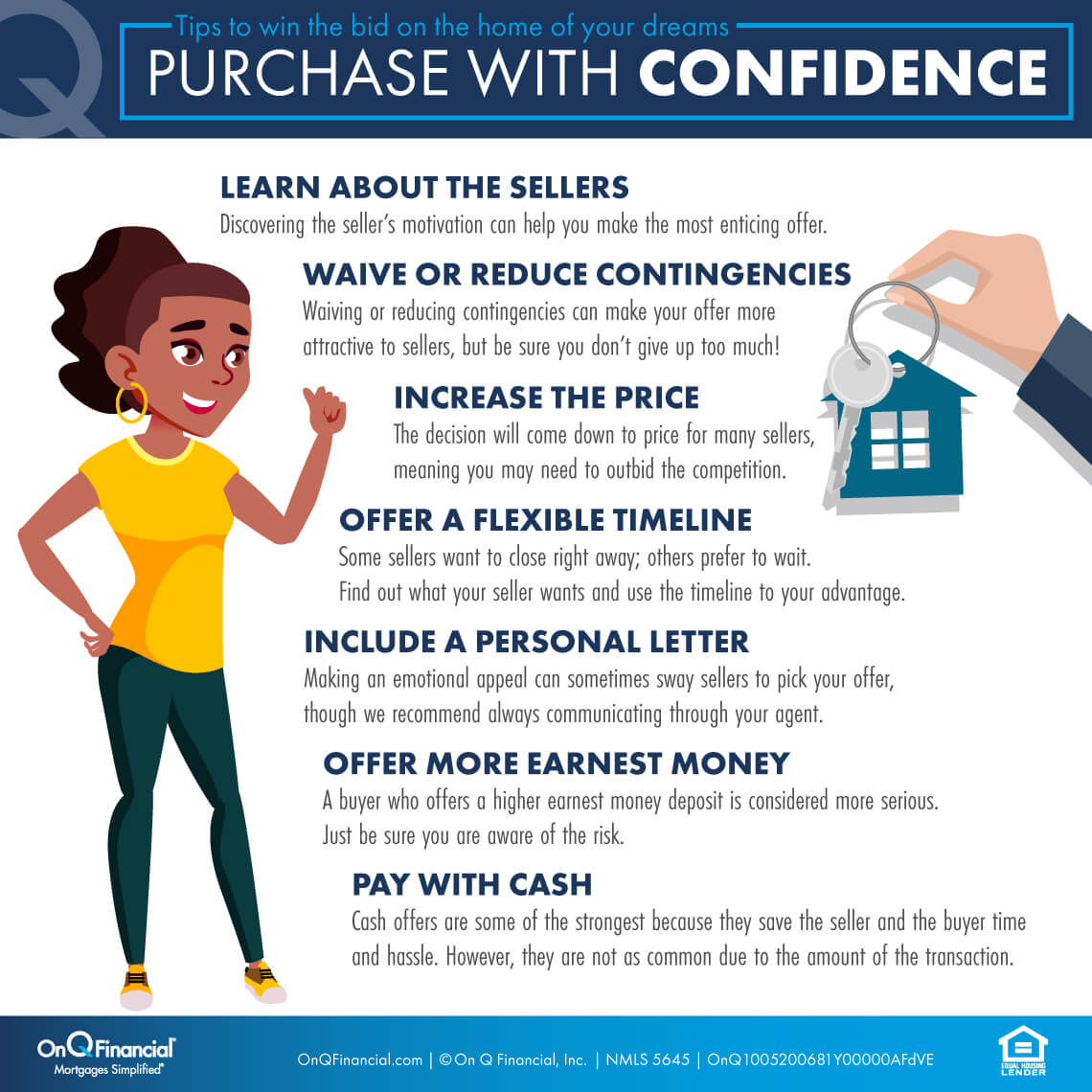

The best offer for some sellers comes down to the most cash. Cash offers themselves are extremely competitive though not always viable for most buyers.

If you are sure this is your dream home, you will want to discuss with your realtor how much you want to offer to ensure it is accepted. In a seller/s market, there may be many buyers bidding on the same home or a “multiple offer” situation.

But there are some things you can do to help you make the best offer.

Finding out why a seller is selling their home may give you some insight into making a better offer. If they are in a rush to close, they may be willing to take a lower offer, provided it doesn’t contain a lot of contingencies that would slow the process. The seller may be looking for flexibility, such as staying in the home a few extra days to move into their new home. Whatever their motivation is, you may be able to use it to your advantage when putting together your purchase offer.

Contingencies are conditions that must be fulfilled to close the sale of a home. Most buyers include contingencies in their offer as they can range from small items to more extensive conditions.

Because most home purchases are financed through a mortgage, a financing contingency could allow the parties to back out of the deal if a loan is not approved as expected. Financing contingencies also come into play when it comes to the closing date. If the loan is not approved by the closing date, some sellers may back out. Luckily, On Q Home Loans offers an On-Time Close Guarantee, meaning you can be sure your loan will not hold up your dream home purchase!

Another contingency that comes along with a financed mortgage is an appraisal. Lenders need to know that they are making a good investment, and an appraisal requirement ensures that the home’s actual value matches up with the amount they are lending. This also protects the buyer since it means they will not overpay. If the appraisal comes back lower, you may be able to renegotiate for a lower price.

Most buyers will want a home inspection, even if it is not required. A home inspection will give you an idea of the state of the home and may reveal some items that can alter the agreement. This provides the buyer with a chance to back out if they do not like the inspection results or add more contingencies based on the report itself.

Sometimes either the buyer or seller will have a contingency based on the sale of their current home. For example, one party might agree to a purchase contract, but only if their own home sells. These contingencies usually hold up the process, so be aware of the seller’s situation. If they want a quick sale, they may be reluctant to agree to this contingency.

While waiving contingencies can make your offer more attractive, consider what you are giving up. Many contingencies are included to protect the buyer, so make your decision carefully and consult your real estate agent or mortgage consultant if you are not sure.

Your earnest deposit assures the buyer of your commitment to the purchase agreement. Neither party can access the earnest money until the transaction is finalized. Until then, it sits in a third party account in case the deal falls through. The amount of your deposit is generally 1-3% of your loan amount, but offering more can sometimes convince a seller of your commitment to purchase their home.

Keep in mind that this will also put you at higher risk if the deal does not go as expected. You will need to rely on any contingencies if you hope to get your earnest money back in that situation. If everything goes to plan, though, your earnest money will be returned or applied to your closing costs, depending on your terms.

Before submitting your offer, ask your agent about “Comps” or a comparative analysis of the home. This analysis will help you decide on your best offer. If you want to guarantee your offer is accepted, you can include an escalation clause within the purchase contract. An escalation clause will allow you to limit how high you are willing to go on an offer if you are outbid. However, you will need to make sure this amount lines up with your loan approval.

The purchase or sale of a home can be a personal and emotional experience. Appealing to the seller directly can sometimes convince them to sell to an enthusiastic buyer. You might include points such as why you love the home or your plans for it.

However, in most cases, we recommend communicating with the seller through your agent. Communicating directly could affect your transaction in ways you may not expect if the communication does not go as planned.

Depending on your willingness to compromise and your seller’s willingness to sell, the time to negotiate will vary. Before you start negotiating, though, think about the market. Your agent will be able to give you an idea of how fast or slow homes are selling in your target neighborhood and will help you determine whether negotiating is a good idea. Consider the leverage you have as a buyer as well, such as how long a home has been on the market or lack of other offers.

Generally, you can negotiate on price, closing timeline, contingencies, and concessions. You can also ask the seller to lower the purchase price in exchange for something like the following:

Submitting an offer for less than the asking price is a significant risk but could result in a big payoff. Be careful not to insult your seller. Speak with your realtor and decide whether offering below asking is a good idea for your specific situation. In most cases, the seller will decline the offer, and you can move on, though keep in mind that in some extreme cases, the seller may refuse to sell to you if the offer was too low.

The legal requirements for a home purchase offer vary from state to state, so you will want to do your research if you aim to buy a home without an agent. All of the necessary documents you need for your home purchase can be found online; however, be extremely cautious as a small mistake could cost you your earnest deposit or more in penalties.

We do not recommend shopping for a home without a realtor or real estate agent. It is best to trust the expertise of industry professionals on such a big decision.

Once you’ve made your purchase offer and it has been accepted, you are ready to move onto the final stages of your Home Buying Journey! Next, you will move into the inspection period and begin any inspections for the new home. When you are ready, continue your Home Buying Journey by learning how to Negotiate Closing Costs.

You now have all of the information you need to purchase your dream home! Before you settle your accounts, continue to the next step of your Home Buying Journey where you will learn how to Negotiate Closing Costs to ensure you get the best deal on your Dream Home!

Next Step: Negotiate Your Closing Costs